Request a Demo

Request a Demo

Background

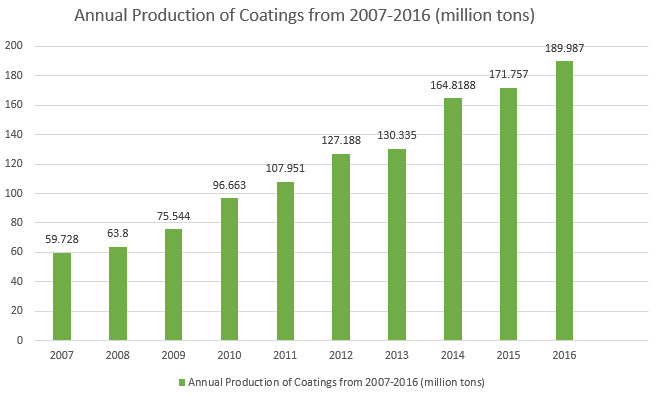

In recent years, China has seen remarkable growth in its coating market. According to China’s State Statistics Bureau (see chart 1), the annual production of coatings has grown steadily since 2007, increasing from 5.9728 million tons in 2007 to 18.9987 in 2016. Moreover, the production of coatings in the first half year of 2017 reached 9.641 million tons, with a growth rate of 10.5% compared to the same period last year.

Chart 1 (figures from State Statistics Bureau)

In 2016, the production volume of industrial coatings was 12.6089 million tons, accounting for 66.37% of overall coating production. The remaining 33.63% was made up by architectural coatings (6.3889 million tons), including interior wall coating (4.09185 million tons) and exterior wall coating (2.29705 million tons).

The water-based coating sector is expected to grow more rapidly in the future. According to Qianzhan research report, the CAGR (compound annual growth rate) of water –based coatings in the 2009-2016 period was 14.08%. In 2016, the national water-based coating production volume was approximately 1.9 million tons, 13% of total production volume. The report also predicted that water-based coating production in 2017 would be 2.32 million tons representing an increase of 22.1% year-over-year.

Regulations on Coatings

Water-based coatings are now a more economical option compared to solvent-based coatings. This is mainly due to favorable policies offered to water-based coating manufacturers/importers such as Consumption Tax on Batteries and Coatings (published on Jan 7th, 2016). Coatings which release less than 420g/L VOCs at worksites are exempted from consumption tax.

Also, China has removed water-based coating waste from the Inventory of Hazardous Wastes (effective since July 2016). This amendment has significantly reduced the production cost of water-based coatings, as hazardous wastes treatment equipment and processing is no longer needed.

China will introduce a negative list which will impact market access across the country in 2018. In accordance with laws and regulations, the negative list clearly states sectors and businesses that are off limits to some market entities. According to the list (term 53), it is forbidden to build new production equipment for titanium dioxide by sulfuric acid method, Lead chromate, iron oxide pigments (less than 10,000 tons/year), solvent-based coating (excluding encouraged types and production process of coatings) and powder coatings with TGIC.

To fulfill environmental-protection requirements in the 13th Five-year Plan, China’s MEP along with other departments released an implementation plan to control and prevent VOCs in September 2017. This plan emphasizes VOCs in industrial coatings, aiming to screen out solvent-based architectural coatings and largely increase usage of water-based coatings in manufacturing containers, automobiles, wooden furniture, etc.

Some provinces and regions have their own policies toward water-based coating:

1. Zhejiang Province

Zhejiang is located in Yangtze River Delta region- one of the production bases of Chinese coating industry. At the end of 2017, Zhejiang has released an Implementation Plan for the Reduction of VOCs (for year 2017-2020). The plan aims to decrease VOCs emission by 20% in 2020 compared to 2015. The following industries are involved: petrochemical industry, industrial coatings, package printing industry, shoemaking industry, etc. Specifically, the focus of supervision in coating industry will lie on coating procedures during manufacturing container, wood furniture, coiled material, steel structure, construction machinery, automobile, and ships.

2. Beijing-Tianjin-Hebei Region

Effective from 1 Sep 2017, Beijing, Tianjin and Hebei province jointly enact the Standard of VOCs limitation for Architectural Coatings and Adhesives. The standard strictly regulates limit requirements for VOCs in architectural coatings and adhesives. It is estimated that VOCs emission will reduce by 20% due to promulgation of the new regulation.

Based on the current legislation and corresponding manufacturers of solvent based coatings are at a significant disadvantage in terms of overall mandatory production costs compared to water-based coating manufacturers . The situation is compounded by increasing public awareness and concern relating to the environmental impact the solvent based coating industry has on the ecosystem.

Features of Water-based Coating Market

1. Potential Expansion

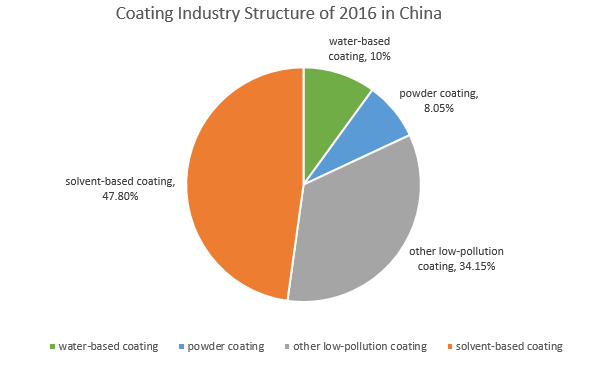

Back in 2009, there was a total of 0.76 million tons water-based coating produced. By contrast, the figure for 2017 is 2.32 million tons, with a CAGR (compound annual growth rate) of 14.08%. Pie chart 2 below shows the Chinese coating industry structure of 2016. Environmentally friendly products (such as water-based coating and other low-pollution coatings) almost account for half of the whole industry. Growth in greener alternatives as a trend likely foreshadows more significant increases in the water-based coating industry.

Pie chart 2 (figures from Qianzhan research report)

2. Limited Market Share

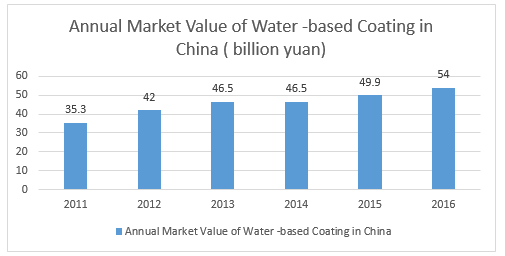

Despite rapid growth, China's water-based coating industry is still relatively underdeveloped. In 2016, the production of water-based coatings was 1.9 million tons which still only accounts for 13% of the total (18.9987 million tons). Compared to 2011, the market value of water-based coating in 2016 increased by nearly 20 billion Yuan. Even though the market value of water-based coating in china is increasing (see chart 3), its market share has never exceeded 15% from 2011 to 2016.

Chart 3 (figures from State Statistics Bureau)

In developed regions such as the U.S. and European, however, more than 80% of automobile primer and 50% of metallictural coatings are water-based. Compared to developedc coating are water-based. In Germany, 93% of architectural coatings are water-based. Compare to developed countries, China still has plenty room to grow.

3. Dominated by Foreign Brands

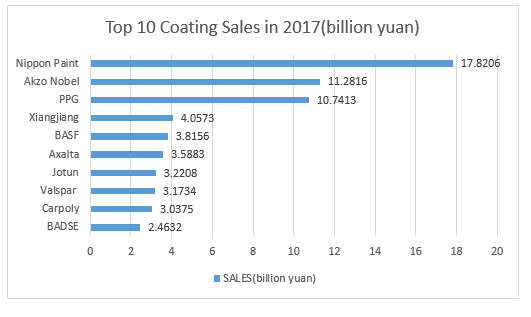

China’s coating market is dominated by foreign enterprises. According to the top 10 coating sales enterprises ranking in China (see chart 4), 8 of 10 are overseas-funded while only 2 are local enterprises- Xiangjiang Paint and BADSE. Noticeably, the top 3 are all from overseas.

Chart 4 (figures from State Statistics Bureau)

In china’s water-based coating market, Chinese producers are less competitive than international brands such as BASF, Axalta, and AkzoNobel. Yet, these international brands are still expanding their capacities in China. Take BASF as an example- at the end of 2017, BASF opened operations in its 140 million euro automotive coatings facility in Shanghai.

Prediction: The Future of Water-Based Coating in China

China still has substantial room for the development of water-based coatings. The increasing demand for environmentally friendly coatings is driven not only by China’s stricter environmental regulations but also by consumer health concerns.

The water-based coating market will continue to grow and more oversea investors will look towards China. Chinese coating manufacturers will need to focus on building technical capacities and production of higher quality products in order to compete with international players.